Targon’s investment methodology, for model portfolios, is quant driven, style agnostic, unemotional and , in the case of Growth 1 Model, constructed with the ‘whole cycle’ in mind.

Diagrams below illustrates aspects of our investment process & what we are thinking now.

Summary:

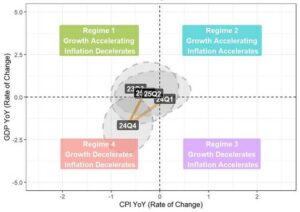

Our forecast for Q4 has changed from a regime 1 where equity would see a positive market environment for returns, to regime 4 which we would normally associated with lower performance for risk assets.

It is important to note that we have predominantly found ourselves in regime 4 in 2024, but risk assets have performed well – on the back of earnings being maintained in the face of decreasing growth.

The “scare” at the beginning of August was on the back of U.S. employment figures dropping. When using the Sahm rule (a prediction tool for recession based on a 0.5% increase in unemployment over the last 6 months) which “triggered” on the non-farm payroll (NFP) figure in August, the market suddenly questioned if the Fed had been too late with the lowering of rates. When using the Sahm rule the probability is 20% for a 20% pullback – but on average the market is expected to remain in positive territory.

The expectation of a Regime 1 has now been moved to Q125 which seems to indicate a view that the remainder of 2024 will be subdued in terms of performance before we get some clarity into 2025.

When considering that the U.S. Election will take place in November, it would seem more likely that we would get a market which would be calm prior to the election and then a rally as the lowering of rates starts getting increasingly priced in.

The main risk over the next month or two is to do with the unemployment – there is a debate among the macro economy fraction and the asset owners (BlackRock and UBS).

The macro economists are arguing that a soft landing is now seriously at risk (Sahm rule among one of the arguments) and that we have a policy error unfolding versus the asset owners which argues that earnings are good and increasing and still believe there is more to come to the upside. Hard not to agree with both arguments.

We are in a market where things are stretched but that does not have to mean we should sell off.

If GDP and CPI are showing a regime 1 or 4 then there should be a greater lean towards tech while commodities related sector and financials are less favoured.

Markets are discounting mechanisms, so prices adjust as expectations adjust.

Forecasts of quarterly regime expectations

NOTE: Regime 1 is optimal for risk assets.

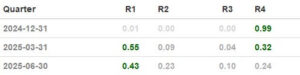

Probability of regimes expectations

NOTE: High probability of Regime 1 Q1-25.

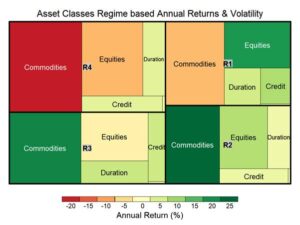

Heat map of returns associated with different regimes

NOTE: The move from R4 to R1 benefits equities over bonds & commodities.

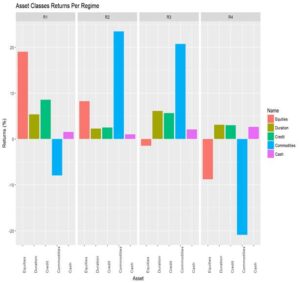

Histogram of expected returns for individual regimes

NOTE: Avoid commodities in R4 and R1.